Let’s face it: nobody likes the closure of a fiscal year. You have to check many things, file mountains of documents and hope you didn’t make a mistake. Thankfully, all this hassle can be reduced radically if you use an online accounting solution. Whether you are ending your fiscal year with or without your accountant, this neat software will give you a helping hand in every aspect you need and will automate as much as possible, so you can concentrate on celebrating another successful business term.

Checks Before Start

The first thing you have to do after you locked out everybody from tampering with the reports, aside from your accountant/financial advisor, is to see all the financial reports and check whether they are all ok. As reports are automatically built, it won’t make any changes unless you do; so if you have to write off bad debts or something is missing, you have to do them manually.

The first thing you have to do after you locked out everybody from tampering with the reports, aside from your accountant/financial advisor, is to see all the financial reports and check whether they are all ok. As reports are automatically built, it won’t make any changes unless you do; so if you have to write off bad debts or something is missing, you have to do them manually.

However, these verifications only take minutes, especially with the help of an expert/accountant.

Closing off Accounts Payable

Approve all the bills issued by your suppliers and attach their invoices to those bills; these steps only require a few clicks and if attachments are uploaded directly to the software’s file storage before the end of year, you can simply search for and attach them quickly. If you have outstanding purchase orders, you can turn them into invoices or bills; however, be sure to decide which invoices you want to pay before the end of year in order to avoid the inclusion of unwanted expenses in your reports.

Closing off Accounts Receivable

If you have drafted invoices or quotes, mark them as sent or send them to your clients if you haven’t done them yet and, in the case of quotes and billable expenses, turn those documents into invoices. If you have created an account where you collect the bad debts, you have made the right choice: you only have to move unpaid invoices to that account and it won’t appear on the reports anymore, thus you have written them off.

Turning Estimates/Quotes into Invoices in FreshBooks

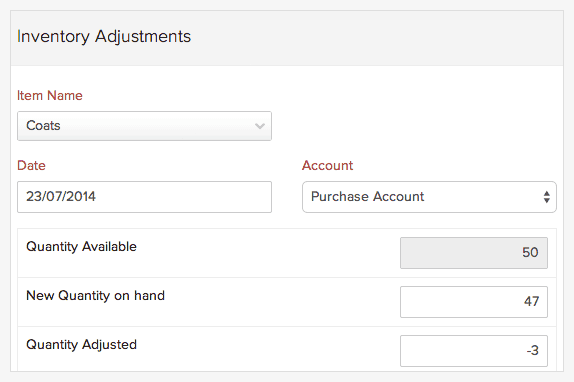

Inventory Adjustment in Zoho Books

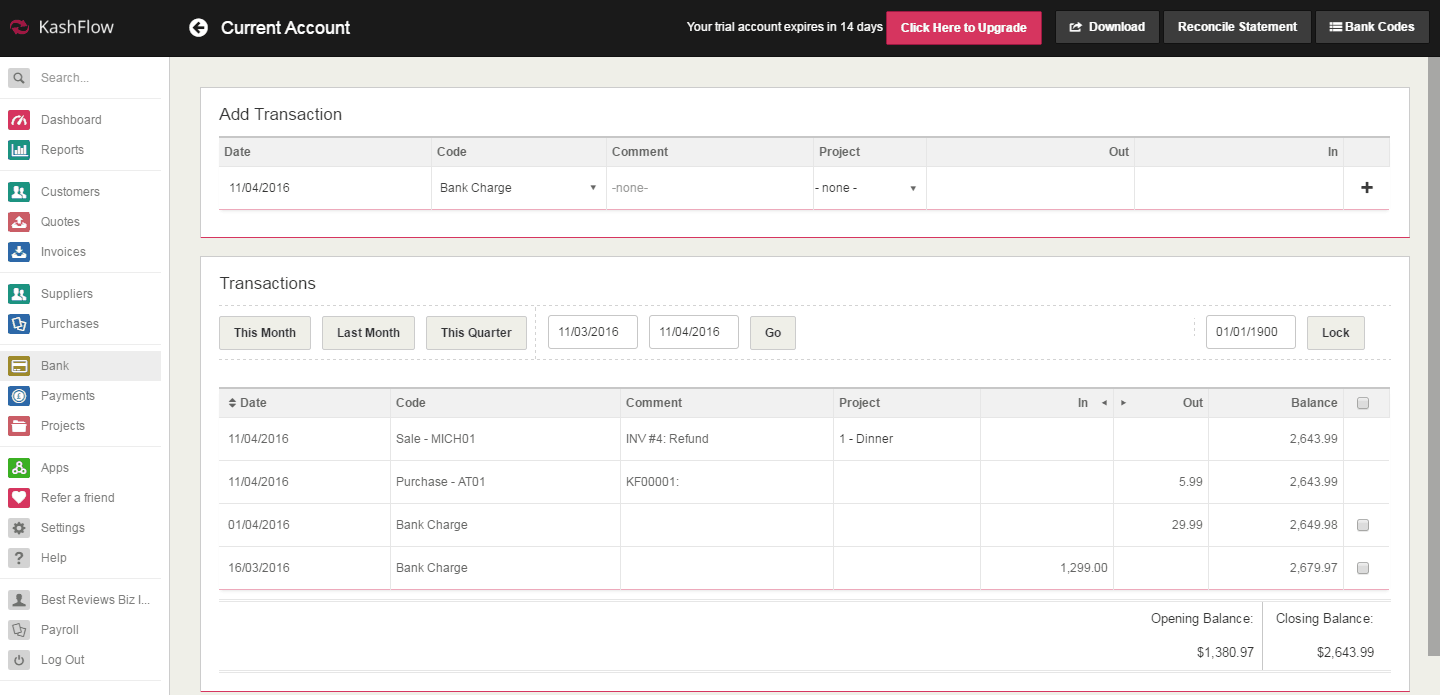

Bank Reconciliation in KashFlow

Inventory and Assets

When you are tracking items in your inventory, you can simply provide new adjustments to the inventory report. For instance, say you have less stock of an item, so you deduce the difference, explain the reason behind the loss and the software will only add the true number of items to the report. With assets you just register the needed ones and delete those that are unnecessary.

Bank Reconciliation

If you have automated bank reconciliation, just check all bank transactions, add the necessary bank statements to your reports and you are done. However, be sure to include all necessary bank transactions, thus if certain transactions are not reconciled or got accidentally deleted, reconcile or reinstate it immediately.

Closure

When everything is checked and then double-checked, you just have to create a recurring journal that will save your reports at the end of each fiscal year. Then simply lock out all other, remaining users from tampering with the reports, publish those papers and voilà, the job is done.

Extra: Further Reading and Learning Materials

If you want to learn more about how to properly end your financial year, you have plenty of options to choose from. For instance, Xero and QuickBooks Online, two of the most popular online accounting solution provider both have neat checklists and how-tos; furthermore, QuickBooks also has a full instruction guide on how to end your year in the software, while Xero has a complete webinar dedicated just to this topic.

Best Online Accounting Software of 2024

| Rank | Provider | Info | Visit |

1

|

Editor's Choice 2024 |

|

|

|

2

|

|

||

|

3

|

|

Get the Best Software and Tech Deals

Subscribe to our monthly newsletter to get the best deals, free trials and discounts on software and tech.

Share Your Comment